Executive Summary

Financial advice, like so many forms of advice, is a uniquely human endeavor. While the internet has a virtually unlimited depth of raw information to access and apply to one’s self, the opportunity to get perspective on your situation from someone else, who can read between the lines and help you recognize what you may not even understand about yourself, requires another human being (ideally one who has a little more expertise than you to help with such realizations). Which, along with the human-to-human accountability that is hard-wired into our brains as herd animals, is what helps financial advisors withstand the threat of robots.

Yet notwithstanding the fact that financial advisors are paid to give advice to their clients in meetings with clients, the latest Kitces Research study reveals that the typical financial advisor spends no more than about 50% on direct client activity-related tasks, and barely 20% of their time actually meeting with clients! In fact, the typical financial advisor spends as much time searching for the next new client (i.e., prospecting and marketing for business development) as he/she does meeting with all their existing clients from week to week. A phenomenon that has only recently begun to shift with the rise of the recurring-revenue fee-based model, that puts less emphasis on continuous business development for new clients relative to the ongoing servicing (and retention) of existing clients.

Still, the fact that so much of an advisor’s time is not spent directly on client activities, and that even the majority of client-related tasks are more “back office” in nature (e.g., client servicing, meeting preparation, and doing various analyses) suggests that there is room for a significant increase in advisor efficiency, either through delegation to staff, better technology, or both.

And fortunately, the data reveals that advisors who delegate to support staff are able to generate significantly more revenue and generate a higher income… except as it turns out, this is largely accomplished by providing more time and more services to clients in the aggregate (between the advisor and his/her support staff), which allows the advisor to move “upmarket” and attract more affluent clients (who each pay a greater fee). Similarly, the rising use of more capable financial planning software amongst advisors doesn’t appear to be generating any time savings efficiencies and instead is being leveraged by financial advisors to go deeper with clients and do more in their financial plans (rather than simply doing the plans faster).

All of which raises the question of whether the limitation on a financial advisor’s time and client-facing activities is really a matter of technology and staff efficiency in the first place or a more “human” limitation on how many relationships any one person – or any one advisor – can manage in the first place. As thus far, the inexorable rise of technology continues to not lead financial advisors to service more clients, but instead to provide more and deeper services to their clients. Which suggests, in the extreme, that ongoing technology efficiencies may not increase advisor productivity, and instead will simply bring down the cost of financial advice and make it more accessible… which in turn will only further exacerbate the existing talent shortage of financial advisors in the coming decade?

How Does A (Lead) Financial Advisor Spend Their Time?

The classic view of a financial advisor is one who gives financial advice – literally, sitting across from clients, dispensing out financial wisdom.

Yet the reality is that financial advisors don’t only meet with clients to give them financial advice. There is also work in analyzing their financial situation to give the advice. And meeting with prospective new clients to earn the right to give them advice. And helping all of them implement the advice. Not to mention running the “advice business” that’s built around the advisor as well!

Accordingly, in our recent 1,000+ advisor Kitces Research study on “How Financial Advisors Actually Do Financial Planning,” we gathered in-depth information on how financial advisors really spend their time across all the domains of what it takes to be a financial advisor.

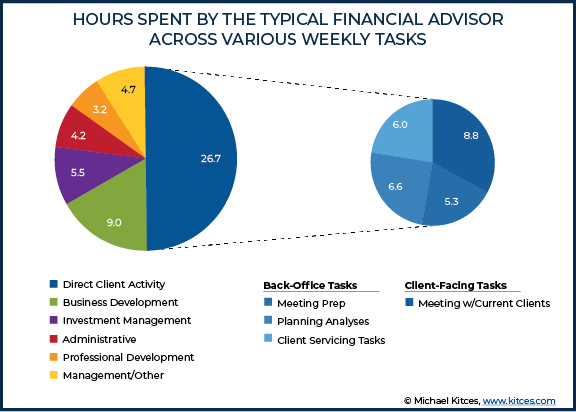

Overall, the average financial advisor (in a “lead” position of being directly responsible for managing client relationships and developing new ones) reports that they spend 43 hours per week working as a financial advisor.

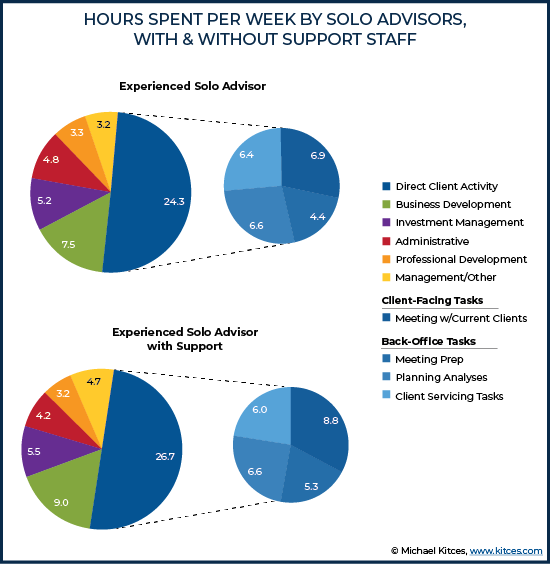

When breaking down the tasks of what they do, the biggest is – not surprisingly – meeting with their current clients, which occurs an average of 8.8 hours per week, plus another 5.3 hours per week of preparation for the meetings, and an additional 6.6 hours per week of doing the supporting financial planning, investment, and other analytical work to answer client questions (either in advance of meetings, or in response to client inquiries that come in via telephone or email). Which in turn creates an average of 6 hours of follow-through client servicing tasks. In total, the average advisor spends 26.7 hours on these direct client activities.

The next most time-consuming domain for advisors is getting new clients, which consumes an average of 9 hours per week, including nearly 4 hours actually meeting with prospective clients, and another 5 hours of marketing and related business development activities on top.

From there, advisors spend an average of 5.5 hours on investment-managed-related tasks (from investment research to trading and implementation with clients), 4.2 hours on administrative tasks, 3.2 hours on professional development, and 4.7 hours on management and other responsibilities.

All of which, ironically, adds up to 53 hours per week… suggesting that when it all comes together, the typical advisor is struggling with time management and is spending far more time on and in the business than they ever realize!?

Notably, this detailed breakdown of how lead financial advisors spend their time reveals that (only) about 50% of the typical advisor’s time is actually spend on client-related activities – meeting with current clients, or doing meeting preparation, planning analyses, or other client servicing tasks – and less than 20% of a typical lead advisor’s time is actually spent meeting with current clients!

On the other hand, even with a "typical" 1 to 1.5 hour client meeting, this still amounts to the capacity for 6-9 client meetings per week, or 300-450 meetings per year, which is enough to see 100-150 clients an average of 3x per year. And given that the human brain can’t handle more than about 100-150 clients in the first place, this suggests that the typical advisor is making full use of available meeting time and need… and then is simply filling the rest of their available time around it.

In the meantime, the typical lead advisor also still spends just as much time doing business development for new clients (9 hours per week, including both prospect meetings themselves, and other marketing activities like networking or seminars) as they do actually meeting with current clients. While administrative tasks (another 10%), professional development (averaging 3 hours per week), and various management tasks (averaging about 5 hours/week) are cumulatively a minor (but not trivial) portion of an advisor’s time.

Perhaps most notable – at least given the dominance of the AUM model – is that the actual work of “investment management” itself, from doing investment research to the actual trading and implementation, is barely 10% of the typical advisor’s time. In other words, despite the perceptions of some consumers – and regulators – financial advisors who manage portfolios are not sitting in front of computers “managing” the portfolio on a continuous daily basis. In fact, given that the average experienced lead advisor has 96 clients, the average advisor only spends 2.9 hours per year actually “investment managing” the client’s portfolio. (A testimony to the scalable efficiency of today’s trading and rebalancing software tools for advisors and the benefits of centralized or outsourced investment management!?)

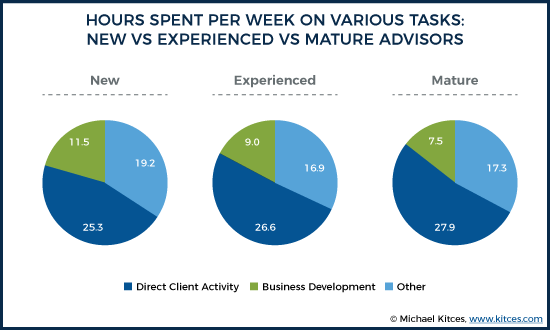

However, these dynamics of how advisors spend their time is also heavily influenced by how many years of experience they have in the first place. As advisors who have been in a client-facing role for more years tend to have more clients to meet with and service in the first place, while those who are newer typically must do more business development because they don’t have clients yet and still need to get them!

Thus, not surprisingly, the data shows that newer financial advisors (up to 5 years of experience) average 21% of their time on business development (almost 12 hours per week) but only 13% (7 hours per week) in meetings with current clients. While more experienced advisors (5-15 years of client-facing experience) spend 17% (9 hours) on business development and 16% (8.3 hours) on client meetings, and the most mature advisors (15+ years of experience) spend just 14% of their time (7.5 hours/week) with prospects but 19% of their time (10.2 hours/week) with their accumulated existing clients.

How Financial Advisors Spend Their Time Differently Across Industry Channels

In addition to the fact that a financial advisor’s time varies by their years of experience – and more directly, by the size and stage of their advisory business itself – the nature of the advisor’s industry channel, and its impact on the advisor business model, also has a significant impact on how financial advisors spend their time.

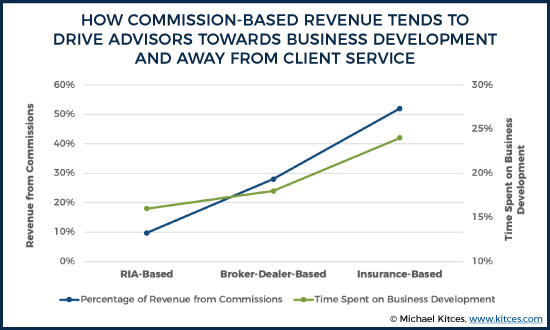

For instance, insurance-based financial advisors that are classically compensated by commissions must start every January 1st with no revenue until they go out and get new clients. Of course, insurance trails and 12b-1 fees, along with the rise of fee-based platforms in insurance broker-dealers, have shifted the insurance advisor’s business model to have at least some recurring revenue. Nonetheless, the average insurance-based financial advisor (working for an insurance company or an insurance broker-dealer) reported 52% of their revenue as commission-based (from insurance or investment products)… and accordingly, spend an average of 24% of their time on business development for new clients (and only 17% of their time meeting with existing clients).

By contrast, broker-dealer based advisors (whether in wirehouses or independent broker-dealers) reported an average of only 28% of revenue from commissions, and perhaps not surprisingly spent “only” 18% of their time spent on business development (and another 18% meeting with current clients). While RIAs reported only 9.7% of revenue from commission-related products (e.g., RIAs with insurance relationships or doing private placements), and spent the least amount of time in business development at only 16%, along with another 16% of their time meeting with clients.

Of course, a greater commitment of time towards business development has to come from somewhere. Though notably, all three channels of advisors do report a fairly similar range of time spent on direct client activity, varying from 48% for insurance-based advisors to 50% for RIAs and 51% for broker-dealers.

The distinction, though, is that these time commitments are distributed across substantively different volumes of clients in the first place.

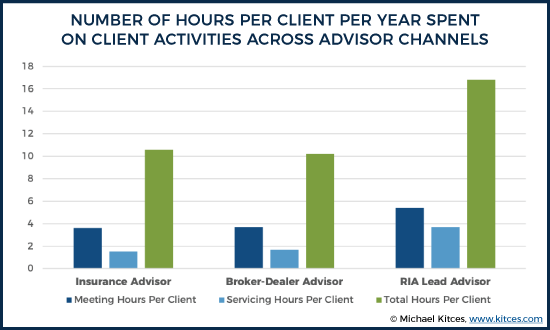

Because as the data shows, the average lead advisor at an RIA is responsible for 71 clients, in addition to 7 new or one-time clients, and has only about half a dozen no-longer-active or dormant clients (e.g., accommodation clients like children of existing clients who did business once in the past but aren’t “active” in the current year). By contrast, the average advisor at a broker-dealer has 118 ongoing client relationships, plus 18 one-time clients, and an average of 31 dormant clients. And the insurance-based advisor similarly has 113 active clients, 14 one-time clients, and 59(!) dormant clients.

Which means that throughout the year, the average RIA lead advisor spends 5.4 meeting hours per client (e.g., 3-4 meetings averaging 1 – 1.5 hours each, or fewer in-person meetings with some phone “meetings” in between), while the average broker-dealer-based or insurance-based financial advisor spends only 3.7 or 3.6 hours (respectively) of meetings per client (averaging 1-2 meetings plus some phone calls each year). In addition, RIAs spend more time on client-servicing task support with clients, despite having far fewer clients (especially including dormant clients that may still have occasional servicing task demands), resulting in an average of 3.7 client servicing hours per client for an RIA, compared to only 1.7 client servicing hours per year for advisors at broker-dealers and 1.5 hours/client/year for insurance-based advisors.

Thus overall, the average RIA spends a cumulative 16.8 hours of direct client activity time per client each year, compared to 10.2 hours/year/client for brokers and 10.6 hours/year/client for insurance-based advisors.

In other words, while advisory firms with predominantly recurring revenue generally don’t need to spend as much time on business development in the long run (as their cumulative number of clients add up and reach critical mass), but still face a limit on the total number of client relationships they can sustain, they tend to fill in the available time by spending substantially more it per client in the ongoing advisory relationship… to the tune of nearly 60% more in direct client activity time per client throughout the year! Or viewed from the other perspective, the greater the commission-based revenue focus of the firm, the more focus on both ongoing business development and a higher volume of shorter interactions with each existing client (ostensibly to find new sales opportunities but not necessarily to engage in deeper financial advice?).

How Paraplanners Spend Their Time Supporting Lead Advisors

Given that less than 20% of a typical advisor’s time is spent actually meeting with clients, while 34% is spent on back-office client work from meeting preparation to doing analyses (plus another 8% on administrative tasks), the question also arises: how can advisors better leverage their time?

The answer, in short, is support staff. Not just at the purely administrative level (which appears to already be well-adopted, given that administrative tasks do comprise less than 10% of the typical advisor’s time), but an associate advisor or paraplanner that can support the other 34% of more-directly-client-related on planning and advice activities.

For instance, when comparing experienced solo advisors (at least 5 years of experience) who are purely solo advisors (entirely on their own) versus those that leverage support staff, the time-usage of advisors looks somewhat different. As not surprisingly, advisors with support staff are able to spend more time meeting with current clients (another 3 hours per week, allowing 1-3 more meetings with clients every week), more time meeting with prospects (another 1 hour per week), and less time doing client servicing and administrative tasks. (Though ironically, advisors with support staff spend more time on meeting preparation, albeit because the total number of meetings rises so significantly as well!)

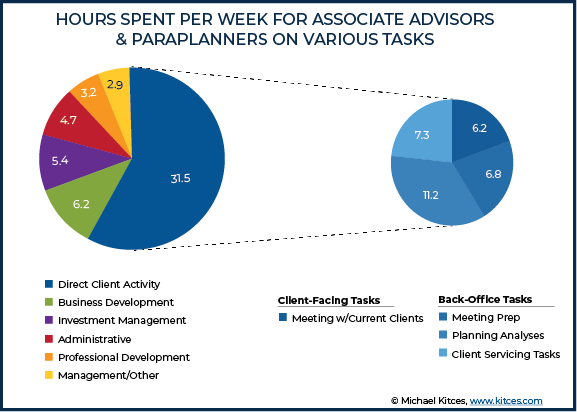

And how do paraplanners themselves spend their time to provide this support work? By spending a lot more time supporting those direct client activities, with an average of 21% of time on planning analyses, 14% on client servicing tasks, and 13% on meeting preparation. In fact, nearly 50% of a typical paraplanner’s total time goes towards these client (and advisor) support activities, along with 12% of time being in meetings alongside lead advisors to further support the process. In other words, paraplanners typically spend more time on direct client activities than lead advisors themselves (albeit less time in actual client-facing meetings)!

Notably, though, for the addition of an entire support staff member to the lead advisor, total time spent by lead advisors on direct client activity is not substantially diminished; instead, it simply shifts slightly towards client-facing meetings and away from the back-office support time, and in fact the total direct client activity time tends to rise when a paraplanner is added to the picture.

The reason, simply put: adding a paraplanner drastically increases the overall capacity of the lead advisor in the first place.

Accordingly, the average lead advisor who operates entirely as a solo has only 73 ongoing clients, while the average lead advisor with a paraplanner services 120 clients (and works approximately identical total hours per week to support those 120 clients!), which in turn leads the average solo advisor to have a net takehome pay of $155k, while the average lead advisor with a support advisor takes home $279k (even after the compensation to the paraplanner themselves).

Of course, to some extent the reality may not be that advisors who hire paraplanners generate more income, but instead that advisors who generate more income can afford to hire a paraplanner in the first place. Nonetheless, the data does clearly show that the use of support staff is capable of making advisors substantially more productive, spending less time on back-office tasks, more time on client-facing activities (for both existing and prospective clients), while not diminishing total client-facing hours of the team in the aggregate.

In fact, clients working with advisors that leverage paraplanners end out receiving a total of 22 hours per year of direct client activity services (between the advisor and the paraplanner), compared to only 14 hours/year from engaging the pure solo advisor. While the lead advisor themselves manages to cut their individual hours per client by nearly 30% (from 14 hours per client per year down to only 10 hours/client/year), and cuts servicing time per client by almost 40% (from 2.9 hours per client per year down to just 1.8), which is made up (and then some) to the client with the associate planner’s support time instead.

In turn, this greater depth of client servicing appears to be effective in allowing advisory firms to attract and retain more affluent clients, with the average advisor with a paraplanner generating $2,850/year of revenue per client, compared to only $1,531/year for each client as a pure solo advisor (even after limited to those who have 5+ years of experience and aren’t just “new” advisors)!

Time Efficiency For Financial Advisors And Clients/Advisor Capacity Limitations

Ultimately, the key takeaway from our Kitces Research study is that, notwithstanding the focus of financial advisors on working with clients and giving financial advice, the typical financial advisor only spends 50% of his/her time on direct client activity, and less than half of that is in the actual process of meeting with clients.

In fact, the ongoing pressure on financial advisors to both service clients and develop new ones – which is only recently beginning to shift with the evolution of more formal career ladders at larger advisory firms – means that the typical financial advisor still spends as much or more time trying to find the next new client as they do meeting with all of their existing clients (except in recurring-revenue models where an advisor’s time begins to shift)! Though still, both of those activities – meeting with current clients, and with prospective clients – still only accounts for 1/3rd of a financial advisor’s time.

In turn, the typical financial advisor still spends more time on back-office tasks for clients, from meeting preparation and planning analyses to client servicing and administrative tasks, than all their client and prospect meeting time put together. A phenomenon that isn’t materially different amongst advisors who hire support staff to delegate such activities… as the end result is simply that financial advisors end out spending less time per client on such tasks, but the same time in total as they serve a larger number of clients, and serve them more deeply (with more total service hours) in the first place.

This phenomenon – that as advisors scale their staff resources, they tend to go “upmarket” and provide deeper services to more affluent clients, rather than increasing the number of clients per advisor – suggests that the real limitation on advisor productivity, and the maximum number of clients that an advisor can serve, really is more a function of what any one human being can maintain in total relationships (a phenomenon known as Dunbar’s Number), rather than merely that being a constraint of modern technology or efficiency. Which helps to explain why financial planners using financial planning software also do not evidence any time-savings by using more advanced financial planning software, and just tend to go deeper with clients instead (using the more efficient software to do more for the same client, rather than doing the same in less time).

This trend also helps to explain why, as investment management tools and technology have themselves improved – to the point that the typical advisor is paid an assets-under-management fee as their primary or sole source of compensation, yet spends no more than 10% of their time on investment management in the first place – financial advisors still haven’t drastically increased their number of clients per advisor over the past 10 years, and instead the typical number of clients per advisor has declined in recent benchmarking studies even as technology is more widely implemented. As once again, technology efficiencies in investment management aren’t leading financial advisors to serve more clients, but to serve the same clients more deeply instead.

Which ultimately raises the question of how the services of financial advisors may continue to shift with the ongoing rise of financial planning software and other “robo” technology in the coming years… is the future really one where financial advisors leverage technology to serve exponentially more clients, or will financial advisors simply continue to evolve ever-deeper (coaching-style?) relationships with their existing clients, adding more value (at lower cost) to each client and creating an even more severe talent shortage of financial advisors in the first place?